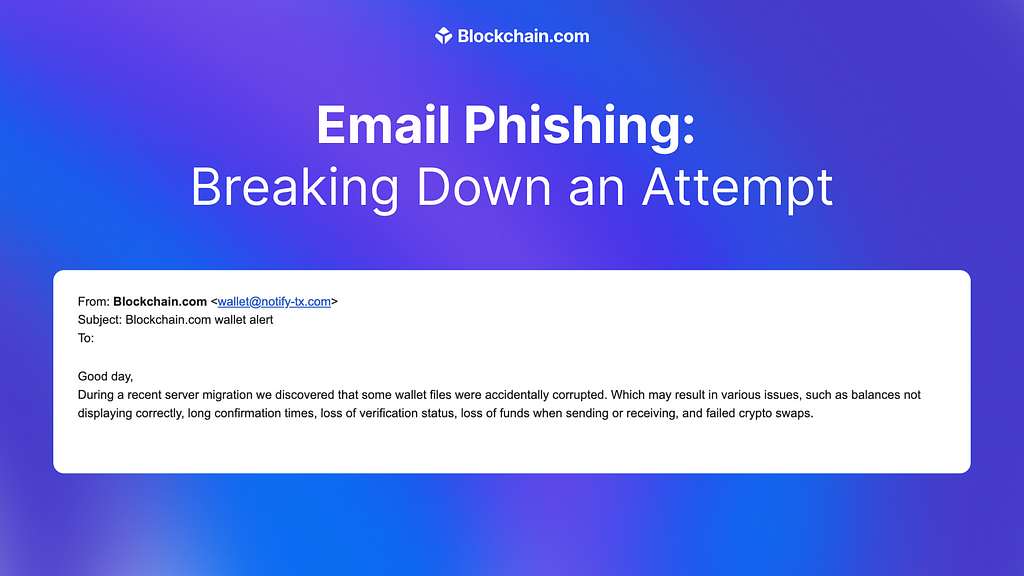

We’ve all received strange emails, an unexpected message from an unknown sender requesting funds or an unsolicited password reset. These emails look genuine, but should we trust them?

Phishing (pronounced “fishing”) is an online attack that attempts to steal your money or identity, by getting you to reveal personal information.

At Blockchain.com we’re committed to help keep you safe online, so in this article we dissect an actual phishing attempt email, highlighting the tactics used.

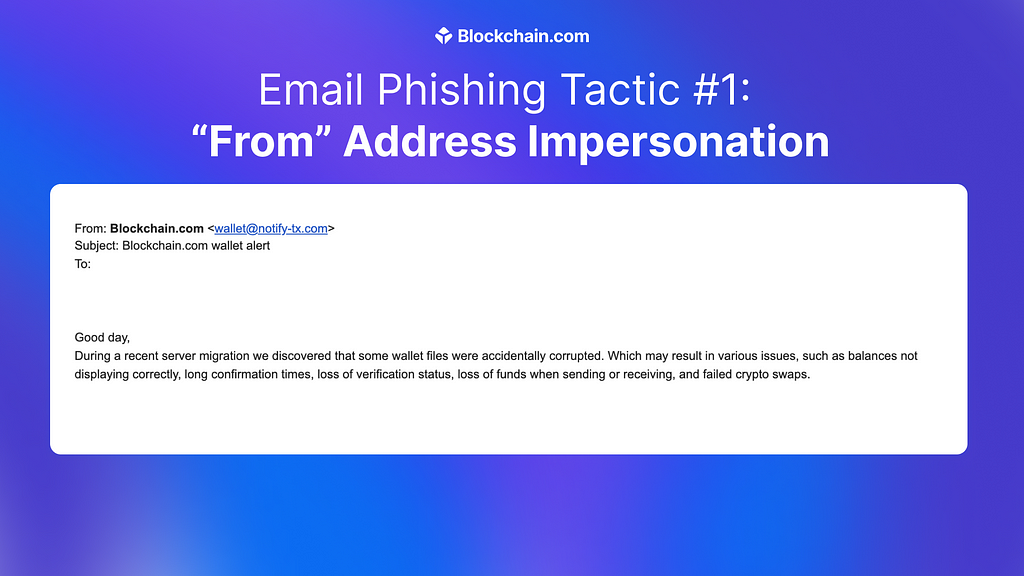

Tactic 1: “From” address impersonation

In this example, the scammer has sent this email from an email address which is similar to our official email address: notify@wallet-tx.blockchain.com

Be vigilant about possible omissions or incorrect characters in email addresses.

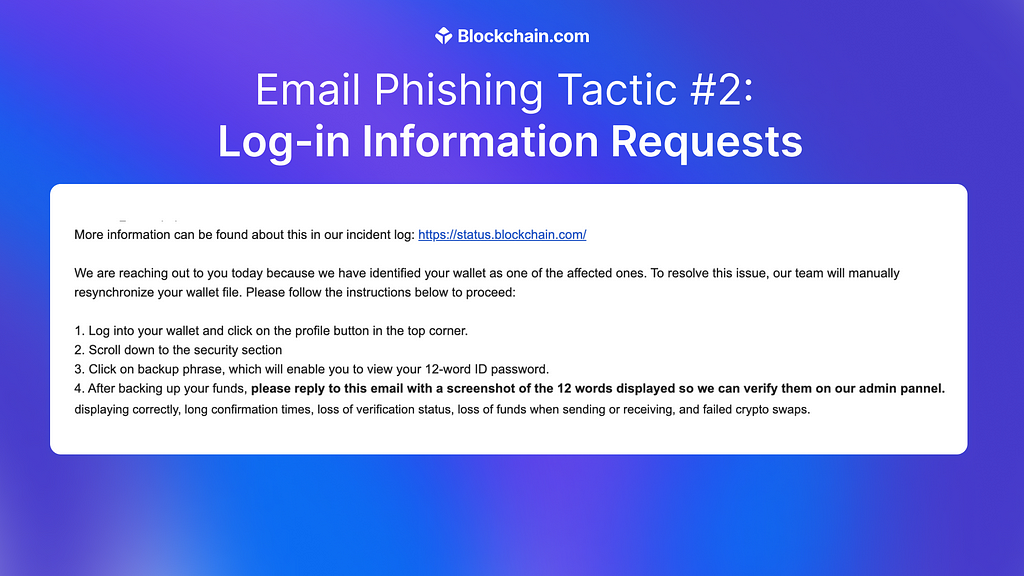

If you get an email or text message (SMS) asking for your Blockchain.com account email, phone, password, or Private Key it most likely is a scam.

We’ll never ask you for login information or recovery phrases in a text or email. This includes:

Credit or debit card numbers

Bank account details

Account passwords

Blockchain.com Private Keys

Blockchain.com Secret Recovery Phrase

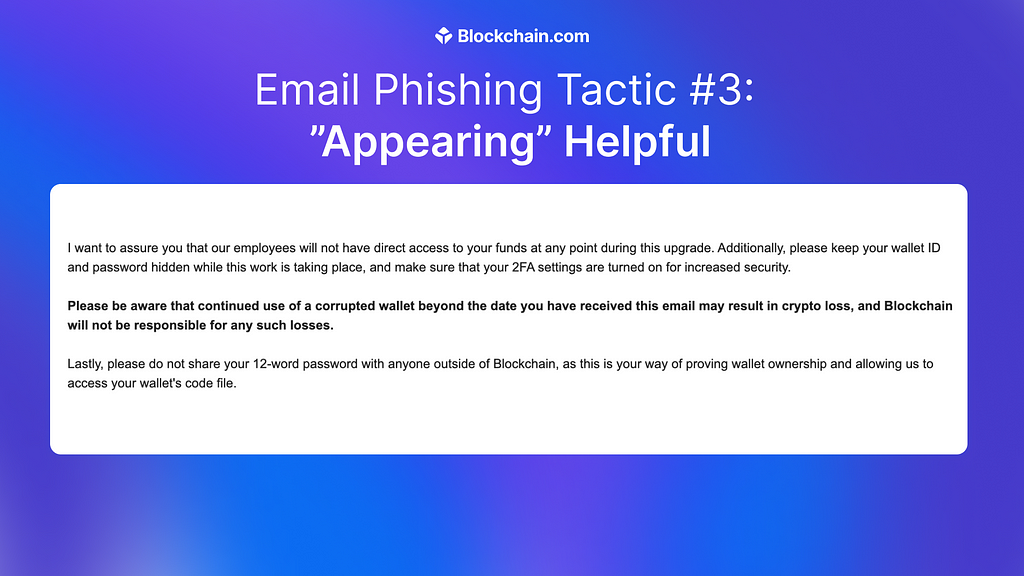

Tactic 3: “Appearing” helpful

See here, the scammer is advising to use 2FA in order to increase security.

We often see scammers sprinkling through what appears to be “helpful” hints and tips as a decoy tactic.

Tactic 4: Using official logos and links

Many phishing emails will consist of standard company logos and official sounding language to make it appear to be real.

While there is no clear way to check if the logo is being used genuinely, it’s important to remain vigilant that scammers will try their best to make the email look as professional as possible.

Phishing attacks are getting more and more sophisticated, with new tactics emerging all the time. The most important thing to remember is that at Blockchain.com, we will never ask for your login information, through any form of communication.

If you have any doubt, open a Support Center Ticket here to confirm the validity of a request.

Today we’re introducing a new way to earn up to 8% annually on your Bitcoin (BTC): Active Rewards.

For those who have a market view on where the price of Bitcoin will go, Active Rewards can be used to maximize your potential rewards at up to 10x the rate of Passive Rewards (formerly “Rewards”).

What is Active Rewards?

Active Rewards provides a way for you to earn on your Bitcoin in an otherwise down or flat market. Specifically, it lets you subscribe to a strategy to earn rewards if you believe the price of Bitcoin won’t go up significantly in the next week.

It could offer a significantly higher rewards rate on Bitcoin than Passive Rewards (up to 8% annually vs up to 0.65% annually, at current rates as of April 2023. To view live rates visit our website).

How does it work?

Every week, a new Active Rewards strategy is made available to all Active Rewards customers that sets a trigger price for Bitcoin that is higher than the current market price. If you believe the price will be under the trigger price at the end of the week, subscribe to the strategy and earn an annual rewards rate on your Bitcoin, paid out weekly on Fridays at 8am UTC.

The trigger price and the rewards rate are set at the start of each weekly cycle and if you don’t withdraw your funds you’ll automatically be rolled into the strategy for the following week.

Since the specific trigger price changes each week, let’s take a look at some scenarios using the following values:

Currency: Bitcoin

Duration: 1 Week

Annual rate: 8%

Current price: $20,383

Trigger price: $22,000

Scenario 1 — Price of Bitcoin is at or lower than the trigger price at the end of the week

If the price of Bitcoin ends the week at or lower than the trigger price, you’ll receive your rewards for the week and your Bitcoin will be returned to you valued at the market price.

So in the scenario depicted below, if you start the week by depositing 1 Bitcoin in Active Rewards, you’d end the week with 1.00147705 which would then be re-subscribed to earn rewards for the following week.

Scenario 2 — Price of Bitcoin is higher than the trigger price at the end of the week

If the price of Bitcoin ends the week higher than the trigger price, you’ll still receive your rewards for the week but your Bitcoin will be returned to you valued at the trigger price, resulting in a reduction in your Bitcoin-denominated balance.

So in the scenario depicted below, you’d start the week with 1 Bitcoin, at the end of the week you’d receive your 0.00147705 Bitcoin reward, but because the price of Bitcoin went over the trigger price your Bitcoin balance would go down from 1 to 0.88147705 Bitcoin. Thus, you’d have a balance of 0.88147705 Bitcoin which would be re-subscribed to earn rewards for the following week.

What are the risks?

While Active Rewards offers compelling weekly rewards on your Bitcoin, weekly market movements above the listed trigger price can reduce your Bitcoin-denominated balance.

How to get started

You can get started by transferring as little as $1 in Bitcoin to an Active Rewards Account:

Log in to your Blockchain.com Wallet using a web browser or a mobile device.

Click Earn in the navigation bar.

Find Bitcoin (Bitcoin) Active Rewards in the table and click Get started.

Select your Bitcoin Trading Account or Bitcoin Private Key Wallet, enter the amount you’d like to transfer, agree to the terms, and add balance.

Your Bitcoin has now been transferred to your Active Rewards Account.

Note: Active Rewards is not available in all countries. You can check your eligibility here.

IMPORTANT NOTE:

The purchase of crypto entails a risk. The value of crypto can fluctuate and capital involved in a crypto transaction is subject to market volatility and loss.

Digital currencies are not bank deposits and are not legal tender. Blockchain.com’s products and services are not subject to any governmental or government-backed deposit protection schemes. Legislative and regulatory changes or actions in any jurisdiction in which Blockchain.com’s customers are located may adversely affect the use, transfer, exchange, and value of digital currencies.

This month, Ethereum will undergo the “Shanghai-Capella” upgrade, the largest network upgrade since the “Ethereum Merge” in 2022.

“Shanghai-Capella” will enable the withdrawal of staked ETH from the Ethereum blockchain, completing its transition from a proof of work to a proof of stake network.

The upgrade promises to usher in a new era of scalability, sustainability and mainstream adoption for Ethereum, but what does it mean for everyday users of Ethereum? Find out below:

When did Ethereum start its transition from a proof of work to proof of stake blockchain?

In September 2022, the “Ethereum Merge” successfully upgraded the Ethereum network’s mainnet from an energy-intensive proof-of-work consensus mechanism to the more energy-efficient proof-of-stake. Proof-of-stake lets users stake cryptocurrency to validate transactions, and in turn these users are rewarded for that participation with cryptocurrency.

The merge, however, did not offer the ability to let individual stakers withdraw deposited Ethereum (ETH) or the rewards generated by those deposits.

This is where the “Shanghai-Capella” upgrade comes into play, as “Shanghai-Capella” will finally enable the withdrawal of staked ETH.

Are Shanghai and Capella two different upgrades?

Technically, yes.

The “Shanghai” upgrade is on the execution side of Ethereum, whereas Capella is the upgrade on the consensus side — taking place straight afterwards.

I haven’t staked Ethereum but I do trade Ethereum, does this mean for me?

Unless you have engaged with Ethereum staking, the upgrade will not change the way everyday users interact with Ethereum.

I have staked Ethereum, how will this impact my Staking account?

You can continue adding to your Blockchain.com Staking Earn Account, but for the first time you will be able to withdraw assets.

We expect withdrawals from your Blockchain.com Staking Earn Account to be available a few weeks after the Ethereum upgrades are complete as the time taken to process withdrawals is set by the Ethereum protocol (not Blockchain.com).

Remember, you remain liable for any taxes in relation to your Staking or other crypto products.

While the upgrade is a huge advance forward for those who stake and the Ethereum network at large, the upgrade will have little impact upon how everyday users interact with Ethereum or the economics of the network itself.

You can track the Ethereum #ShanghaiCapellaUpgrade on the Blockchain.com Explorer

Our Crypto IRL series showcases individuals who are leading the charge in the crypto revolution by using cryptocurrency in real life to drive financial inclusivity, enterprise, and innovation.

We’re excited to share a recent conversation we had with Bernardo Garcia, Co-Founder of Félix Pago, the world’s first chat-bot on WhatsApp that allows Latino immigrants in the US to send remittances abroad.

Félix Pago leverages blockchain and AI to make remittances as simple and fast as sending a message.

Hey Bernardo! Tell us a bit about Félix Pago

Félix Pago serves hard working foreign born Latino immigrants that live in the US and provide support to their family members that stayed in their home country. We leverage blockchain and AI to make remittances as simple and fast as sending a WhatsApp message.

Félix was built to meet Latino’s where they are, on WhatsApp, and to help them save time and money when they take care of their loved ones.

Awesome. And how does Félix Pago use crypto as part of their operations?

Félix leverages stable coins to get the customer’s funds from the US to Mexico.

First, the customer sees a guaranteed exchange rate of USD/MXN in the Félix chat. Once they pay, Félix takes the funds, converts them into stable coins, and then executes the necessary trades in crypto to get the Mexican pesos in the hands of the customer’s beneficiary in real time.

What have the benefits been to the business since introducing crypto?

The main benefits of using crypto are the speed of the transactions and the low costs.

Doing a cross-border transaction via traditional rails, like swift, takes days and is very expensive, which makes it inefficient.

Finally, what do you think the future of crypto holds — in 2023 and beyond!

We believe that the future of crypto is when it powers our day to day lives and we don’t even notice it! That’s what Félix is all about.

In the end, what matters to us and our customers is that the funds get from A to B in real time at the lowest possible cost.

Do you have an example to share of how cryptocurrency is being used IRL? Tweet us! @blockchain

This information is provided for informational purposes only and is not intended to substitute for obtaining accounting, tax or financial advice from a professional advisor. The views, information, or opinions expressed during the Crypto IRL series are solely those of the individuals involved and do not necessarily represent those of Blockchain.com and its employees.

Bitcoin has a frequently cited problem–scalability.

The Bitcoin network can only handle a certain number of transactions at once, making it take a long time for transactions to go through and impacting the price of fees.

One of the leading causes of the scalability problem is that each transaction must be verified by every node in the network, which requires a lot of computational power and bandwidth.

Hal Finney was an American software developer and early adopter of Bitcoin who received the first bitcoin transaction from Satoshi Nakamoto

The Bitcoin network, as it exists now, can’t function as a payments system at a large scale, and it was never meant to.

As a Layer 1 system, the core Bitcoin blockchain serves its purpose as intended: it’s a decentralized, immutable ledger system.

Part of Bitcoin’s store of value comes from the energy required from the Proof of Work consensus mechanism it uses, but this doesn’t translate well to being used as a globally adopted medium of exchange.

Enter, the Lightning Network.

What is the Lightning Network?

The Lightning Network was designed to improve the speed and efficiency of transactions on the Bitcoin network by allowing users to make transactions off-chain without the need for block confirmation on the blockchain.

This can help to reduce transaction fees and improve the overall scalability of the network.

The Lightning Network is a Layer 2 protocol that allows users to create payment channels on the Bitcoin network.

The Lightning Network white paper was written in 2016 by Joseph Poon and Thaddeus Dryja, and has been in active development ever since.

The Lightning Network runs on top of the Bitcoin blockchain, and it uses multi-signature wallets to enable the creation of off-chain payment channels.

This allows for faster, cheaper transactions and the ability to make transactions without waiting for block confirmation on the blockchain.

How does the Lightning Network work?

The Lightning Network allows for the creation of payment channels between users on the Bitcoin network.

These channels can be thought of as a way for two users to make an unlimited number of transactions with each other without having to wait for block confirmation on the blockchain.

You might wonder why this is even necessary, and the reason is simple–scalability. If you’ve ever tried to send a small transaction through the Bitcoin network, you know that it can be slow and expensive.

Here’s why:

Every transaction that occurs is broadcast to every node on the network

The Bitcoin network processes around seven transactions per second

Network congestion means that only those paying the highest fees are validated

Block validation takes ten minutes due to Bitcoins network protocol

As you can see, this limits the ability to use BTC for micro-transactions.

If you tried to use BTC to pay for your $30 dinner, you could potentially pay an equal amount in fees to process that transaction, plus it would take at least ten minutes for the restaurant to process the purchase.

Compare this with a payment processor like Visa, which can handle around 65,000 transactions per second with nominal fees, and it becomes clear that another solution is needed to make BTC a true medium of exchange.

The Lightning Network solves this using payment channels, a way for bitcoin to be exchanged between users off-chain, or outside of the core blockchain. Users can transact with each other as much as they want, and close a payment channel when they’re done transacting.

The only transactions that are added to the Layer 1 blockchain are the opening (funding) transaction and the closing (settlement) transaction.

Because of this, it’s possible that the Lightning Network could process up to 1 million transactions per second.

To create a payment channel, two users must deposit some bitcoin into a multi-signature wallet on the Lightning Network.

This creates a “channel” between the two users, which can be used for any number of transactions.

Once the channel is created, the users can make transactions with each other by updating the smart contract with the new balance. Both parties sign any updates, but they’re only broadcast to the network once the channel is closed.

When the channel closes, the final state of the smart contract is broadcast to the Bitcoin network, and the appropriate amounts of bitcoin are transferred to the users’ wallets. This allows for off-chain transactions to be made quickly and without the need for block confirmation, which can significantly improve the speed and efficiency of the network.

The Lightning Network also allows for the creation of multi-hop payment channels, where a user can make a payment to another user through a series of intermediate channels, which in this case is other users on the network. This can further increase the flexibility and scalability of the network.

Using intermediaries is where the Lightning Network really shines, since it further scales payment options.

Here’s how it works:

In this simplified example, there are three people who all use the Lightning Network.

User A and User B have an open payment channel, and User B also has an open payment channel with User C. Users A and C do not have a payment channel established, but they can transact with each other through User B.

No additional payment channel was needed, and the individual off-chain ledgers were all updated throughout the process.

Is the Lightning Network decentralized?

For the most part, the Lightning Network is a decentralized protocol. This means that the Lightning Network is not controlled by any single entity but relies on a distributed network of users.

The decentralized nature of the Lightning Network allows users to make transactions directly with each other without the need for custodians, like a bank or centralized payment processor. This can help to reduce transaction fees and improve the overall speed and efficiency of the network.

Benefits of the Lightning Network

There are several benefits to using the Lightning Network for transactions on the Bitcoin network, including:

Faster transactions.

Lower transaction fees.

Increased scalability.

Greater flexibility.

The Lightning Network has the potential to significantly improve the speed, efficiency, and scalability of the Bitcoin network.

While it’s still in the early stages of development, it has the potential to become an influential part of the Bitcoin ecosystem.

Drawbacks the Lightning Network

As a relatively new technology, the Lightning Network may face some challenges and potential problems. Some of the key challenges and potential issues with the Lightning Network include the following:

Limited adoption.

Complexity.

Security risks.

These challenges and risks should be considered before using the Lightning Network.

Is the Lightning Network the future of Bitcoin?

The Lightning Network has the potential to be an indispensable part of the Bitcoin ecosystem, but you don’t need to use the Lightning Network to start buying BTC.

This information is provided for informational purposes only and is not intended to substitute for obtaining accounting, tax or financial advice from a professional advisor.

The purchase of crypto entails risk. The value of crypto can fluctuate and capital involved in a crypto transaction is subject to market volatility and loss.

Digital currencies are not bank deposits, are not legal tender, and are not backed by the government. Blockchain.com’s products and services are not subject to any governmental or government-backed deposit protection schemes.

Legislative and regulatory changes or actions in any jurisdiction in which Blockchain.com’s customers are located may adversely affect the use, transfer, exchange, and value of digital currencies.

The Lightning Network, Explained was originally published in @blockchain on Medium, where people are continuing the conversation by highlighting and responding to this story.

We’re already a few weeks into tax season! For many people with complicated returns, tax prep started well before January. But even if your situation is fairly simple, you would still need to gather documents, review your finances, and account for any big changes that may have happened over the past year.

Are you ready for tax season? What documents do you still need, if any? Are you filing your own taxes or hiring someone to do it?

Tell us whether you’re ready for tax season and we’ll enter you in a drawing to win a $20 Amazon Gift Card!

Win 1 of 3 $20 Amazon Gift Cards

We’re doing three giveaways — here’s how you can win:

Contest ends Monday, February 24th at 11:59 p.m. Pacific. Winners will be announced after February 24th on the original post. Winners will also be contacted via email.

This promotion is in no way sponsored, endorsed or administered, or associated with Facebook or Twitter.

You must be 18 and U.S. resident to enter. Void where prohibited.

Good Luck!

Tell us whether you’re ready for tax season and we’ll enter you in a drawing to win a $20 Amazon Gift Card!

Preparing for tax season often seems more like a sprint than a marathon. You receive your W2 forms in the mail in late January, and then it’s time to excavate your receipt shoe box and spend a stressful weekend trying to make sense of your tax return. All in all, it feels like a hurried, overwhelming, and nerve-wracking chore that you dread every year.

But what if filing your taxes didn’t have to be quite so stressful?

The trick to making your tax season a breeze is preparing for it early. As in, right now. If you want an easy and relaxed tax season, here’s what you can do now to get ready.

Make a list of the information you’ll need

One of the most frustrating moments in tax preparation is discovering you’re still missing one vital piece of information after you’ve gathered everything you thought you needed. And it’s even worse if you don’t know how to find the missing information.

So look over the specific info you need to file now, to give yourself time to gather all the items well before Tax Day. Specifically, you’ll need:

A copy of last year’s tax return

The Social Security or Tax ID number of every member of your household

The income records of every member of your household

Receipts for your deductible expenses

Records of any taxes you’ve paid throughout the year

Putting together your list of necessary information and checking each item off as you gather it will ensure that you’re fully prepared when you finally sit down to file. (See also: The 7 Most Common Tax Questions for Beginners, Answered)

Organize your receipts

Keeping track of tax-related receipts throughout the year is one of the most difficult parts of handling your taxes. Many people throw all of their receipts for work-related expenses, charitable donations, mortgage payments, medical expenses, and interest statements in a single folder or box to deal with “later.”

Now is an excellent time to dig out your receipts and start organizing them according to category. Having your receipts neatly separated now will make it easy to sort the last few that come in as the year comes to a close, and can help you get into the habit of putting them in order as you receive them.

Gather your paystubs together

Though the majority of filers will receive either a W2 or 1099 form from their employer(s), it’s still a good idea to gather your paystubs before the end of the year to get a rough idea of your income. That will help you identify any potential mistakes on your W2 or 1099 forms as soon as they arrive. It’s far better to catch a mistake early rather than find you need to request a corrected form close to the IRS deadline.

Plus, checking over your paystubs all at once gives you a chance to take a look at your federal and state tax withholding over the year, as well as any pretax contributions you’ve made to your 401(k) or IRA.

Review your W4

Another great reason to look at your paystubs now is that it gives you a chance to review your W4 with your employer.

The W4 form determines how much tax withholding is taken from each paycheck. If you expect to receive a large refund this year, you can adjust your withholding allowances now to ensure that more of your paycheck will come home with you in 2020. If, on the other hand, you worry that you may owe money because you didn’t have enough withheld, now is a good time to adjust your W4 to be sure you don’t have the same problem in the coming year. (See also: Are You Withholding the Right Amount of Taxes from Your Paycheck?)

Send more money to your retirement fund

If you have access to a tax-deferred retirement account like a 401(k) or an IRA, now is the time to see how much money you have set aside this year, and try to increase that number.

As of 2019, workers under 50 years old can save up to $19,000 in a 401(k) and up to $6,000 in an IRA. And every dollar you put into these kinds of accounts reduces the amount of income you have to pay taxes on.

Now is an excellent time to try to maximize your 2019 contribution. You have until the end of the calendar year to maximize your 2019 401(k) contribution, but you can continue contributing to your 2019 IRA until April 15, 2020.

Getting into the habit of increasing your contribution now can also help you reach the maximum in 2020, which is going up to $19,500 for 401(k) accounts, although the IRA maximum will hold steady at $6,000. (See also: 8 Tax Return Mistakes Even Smart People Make)

Plan ahead for your refund

If you expect to receive a refund this year, start thinking about the best way to use the money now. We tend to think of a tax refund as “free money,” even though it’s just your own salary being returned to you. But with a free money mindset, it’s very easy to go overboard spending the refund on fun stuff, like a vacation or a new gadget.

There’s nothing wrong with enjoying your tax refund, but taking a hard look at your budget and finances now can help you to determine if having fun with your refund is the best use of the money. Is there some debt you could pay down (or pay off) with the refund instead? Or is there a major goal you’re saving toward — like a down payment on a house — that would benefit from an injection of cash?

Thinking through the best use of your tax refund before you have it in your hot little hands makes it more likely you’ll make good decisions with it. Once you have the money in your possession, it’s very tempting to make it rain instead of saving for a rainy day.

Make your tax season less stressful

Getting a jump start on your filing chores will not only make tax season much easier, but it can also help you prepare for your finances in the coming year. Start 2020 on the right financial foot by starting your tax season preparation early.

Editor’s Note: Congratulations to P, Samantha, and Tabathia for winning this week’s contest!

You don’t want to get your taxes wrong, but if your finances are fairly simple and you’re usually pretty organized, it’s pretty safe to file taxes on your own.

Do you file your own taxes? What do you think is the most complicated part of the process? What advice would you give to someone who is filing their own taxes for the first time?

Tell us whether you file or own taxes and we’ll enter you in a drawing to win a $20 Amazon Gift Card!

Win 1 of 3 $20 Amazon Gift Cards

We’re doing three giveaways — here’s how you can win:

Contest ends Monday, February 25th at 11:59 p.m. Pacific. Winners will be announced after February 25th on the original post. Winners will also be contacted via email.

This promotion is in no way sponsored, endorsed or administered, or associated with Facebook or Twitter.

You must be 18 and U.S. resident to enter. Void where prohibited.

Good Luck!

Tell us whether you file or own taxes and we’ll enter you in a drawing to win a $20 Amazon Gift Card!

Welcome to Wise Bread’s Best Money Tips Roundup! Today we found articles on tax secrets of the rich, ways to adopt a zero-waste lifestyle, and household chores you should outsource.

8 Ways to Adopt a Zero-waste Lifestyle — It’s not easy to achieve a zero-waste lifestyle, but it is possible with a little dedication and some really good tips. [No Sidebar]

Insider Tips For Saving Money on the Great Summer Road Trip — Accidents, construction, and road closures can happen on any route, but you’ll save time, gas, and patience by planning some backup routes just in case. [PopSugar Smart Living]

How to Stock a Home Bar on a Budget — Booze tends to see the highest markup whenever you go out for food or drinks. If you’re deliberate and patient, you can stock up your home bar for a fraction of the price you would spend at a bar. [Money After Graduation]

How to Write a Professional Work Email — The lack of verbal cues can cause misunderstandings in emails. Use this simple guide to help you handle your electronic correspondences like a pro. [Daily Worth]

In 2017, the IRS received 152,235,000 tax returns — and of those returns, more than 73 percent were granted a refund. With the average refund last year standing at $2,895, you might think getting a windfall in the spring is a good thing. But rather than giving the government an interest-free loan all year, wouldn’t you have preferred to have an extra $241.25 per month in your paycheck?

On the other hand, the 27 percent of taxpayers not receiving a refund may be getting the opposite — a big tax bill. They may not be having enough money withheld from their paychecks for taxes.

This is why it’s important to withhold the right amount of taxes out of your paycheck. Let’s review how to cover your projected tax liability while minimizing your refund. (See also: Bigger Paycheck or Bigger Tax Refund — Which Should You Pick?)

Meet the IRS Withholding Calculator

With the passing of the Tax Cuts and Jobs Act, many Americans are still trying to figure out the full effects of this legislation on their paychecks. In an effort to help taxpayers make sense of recent changes to the tax law, the IRS updated its Withholding Calculator on February 28, 2018.

While the IRS recommends that all taxpayers take a second look at how much in taxes they’re taking out of their paychecks, the agency highly encourages the following groups to check their withholdings for 2018:

Two-income families.

People with two or more jobs at the same time or who only work for part of the year.

People with children who claim credits such as the Child Tax Credit.

People who itemized deductions in 2017.

People with high incomes and more complex tax returns.

How to use the IRS Withholding Calculator

Here’s your game plan to achieve a “Goldilocks” withholding rate on your paycheck this year.

1. Gather your latest pay stub(s) and latest tax return

If you don’t receive a pay stub in the mail, contact your human resources office to get a copy or learn how you can download one online from your company portal. Depending on your unique financial situation, you may also want to find your 2016 return (or your 2017, if you’ve completed it) to more accurately estimate your 2018 income, budget, expenses, and list of tax credits.

2. Provide general information and list potential tax credits

In the first two sections of the IRS Withholding Calculator, indicate your filing status, whether or not anybody can claim you as a dependent, how many jobs you and your spouse (if applicable) have, how many dependents you will claim on your return, and whether or not you or your spouse will be 65 or older on January 1, 2019.

Additionally, you will need to list any applicable tax credits, such as the Child Tax Credit and Earned Income Tax Credit. This is why it’s helpful to have past returns handy to help you estimate those credits. (See also: 8 Tax Return Mistakes Even Smart People Make)

3. Detail your wage income and withholding

Next, enter your gross wages, salaries, tips, and any bonuses you expect to receive in 2018. Using your most recent pay stubs, enter the total federal income tax withheld to date in 2018 and the federal income tax withheld from your last salary payment. Indicate how frequently you receive your paychecks, and, if applicable, when you started this job in 2018, and when you expect this job to end in 2018.

If you receive any other taxable income, make sure to include it as well. The IRS Withholding Calculator is only as accurate as the information you enter, so leaving that income out may result in a higher tax liability.

4. List deductions

Here is one of the biggest changes implemented by the Tax Cuts and Jobs Act. If your standard deduction ($12,000 for individuals, $18,000 for heads of household, and $24,000 for married filing jointly) is more than your total itemized deductions, your standard deduction will be used to calculate your withholding. Otherwise, your total itemized deduction amount will be used. So, this is why it still pays to keep track of all of those deductions throughout the year.

Use your latest return to estimate your 2018 itemized deductions, including medical and dental expenses, paid taxes (up to $5,000 for single filers and $10,000 for married filers for applicable state and local income taxes, property taxes, or sales taxes), gifts to charity, and other itemized deductions. Remember that beginning in 2018, job and certain miscellaneous expenses are no longer deductible. (See also: 12 Things You Should Know About the New Tax Law)

5. Adjust your W4

Once you have entered all the data, the IRS Withholding Calculator will provide you with clear instructions on how to update your W4 with your employer. Depending on your situation, some action items may include changing your filing status, adjusting your number of allowances, and withholding an extra amount every paycheck.

Following the instructions from the calculator, you’ll cover your tax liability just right.

Revisit the IRS Withholding Calculator as necessary

Don’t set it and forget it. If your job (Promotion? Salary bump? Side gig?) or life situation (Married? Baby?) changes, revisit the IRS Withholding Calculator. The calculator will help you make sure you have the right amount of tax withheld from your paycheck at work.

The IRS recommends submitting your updated W4 to your employer as soon as possible. Withholding takes place throughout the year, so it’s better to take this step right away.

{kind=link}

{kind=link}